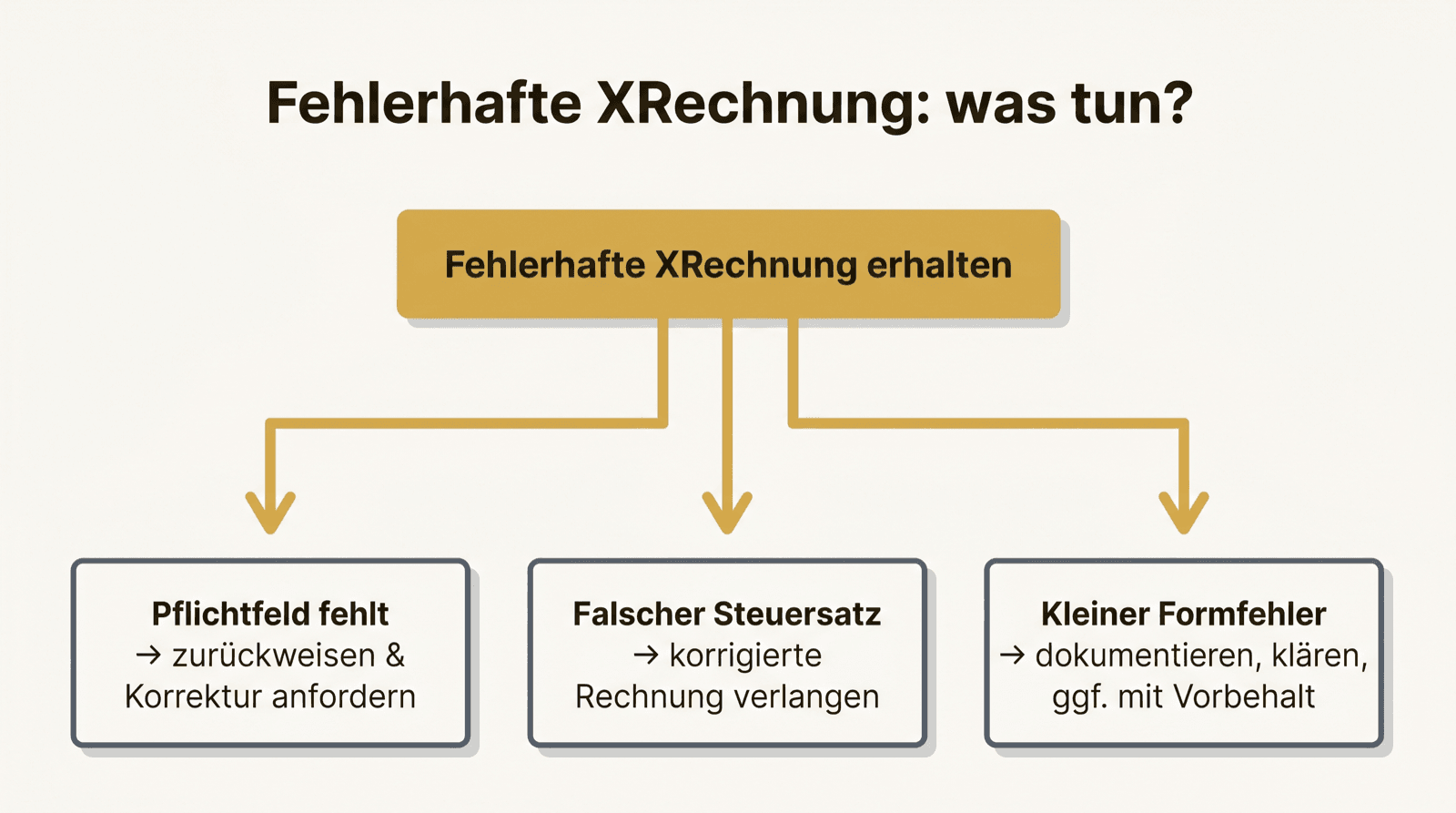

First clarify: what exactly is faulty?

“Faulty” is not equal to “faulty”. A missing VAT mandatory field is something different from a nice-but-irrelevant detail. Before you react, the classification is worth it: technically invalid, factually wrong or only cosmetically unattractive?

These three cases lead to three different reactions — there is no blanket answer.

Missing mandatory field: reject

If a VAT mandatory detail is missing — e.g. the tax number, the service date or a complete address — the invoice is not proper. Here the clean reaction is to request a corrected invoice.

The reason is tangible: an improper invoice can endanger the input-VAT deduction. Posting anyway out of convenience saves minutes today and may cost real money later.

Wrong tax rate or amount: have it corrected

If the tax rate is wrong or the totals do not add up, a correction by the supplier is the right way — not a silent adjustment on your side.

“Fixing” a factually wrong invoice yourself creates a difference between document and posting. Exactly that shows up in an audit. Better to ask once than to drag along an inconsistency permanently.

Minor formal error: document and clarify

Not every blemish justifies a rejection. Some defects are curable or harmless. Here the pragmatic way is: document the error, clarify it with the supplier and record traceably how it was decided.

What matters is not that an error never occurs but that it stays traceable how you dealt with it. That is exactly what a later audit expects.

The rule behind all three cases

One line runs through it:

- Do not post faulty invoices silently.

- Do not delete faulty invoices silently.

- Detect the error, document it and clarify it with the supplier.

- On mandatory defects insist on a corrected invoice — ideally before payment.

- Record the decision path traceably.